If you have ever opened your insurance paperwork and seen a one or two page summary at the very front, you have already met your declarations page. It is the single most useful page in your entire policy, yet most Georgia homeowners and drivers glance at it once and file it away.

What a declarations page actually is

A declarations page, often shortened to "dec page," is the cover-sheet summary of your insurance policy. Your full policy can run 40 to 80 pages of legal language describing what is covered, what is excluded, and how claims are handled. Almost nobody reads all of that. The declarations page pulls the handful of facts that are specific to you and puts them in one place: who is insured, what property or vehicle is covered, how much coverage you bought, what it costs, and when the policy runs. Think of it as the dashboard for your policy. The engine is the full contract behind it, but the dashboard tells you, at a glance, what you are working with.

Every standard policy in Georgia has one, whether it is for a house, a condo, a rental, a car, a boat, or a business. The format varies a little from one company to another, but the core information is the same. If you ever need to prove you have coverage, apply for a mortgage, settle a claim, or compare quotes, the dec page is the document people ask for.

The main parts of a declarations page

While layouts differ, nearly every dec page contains the same building blocks.

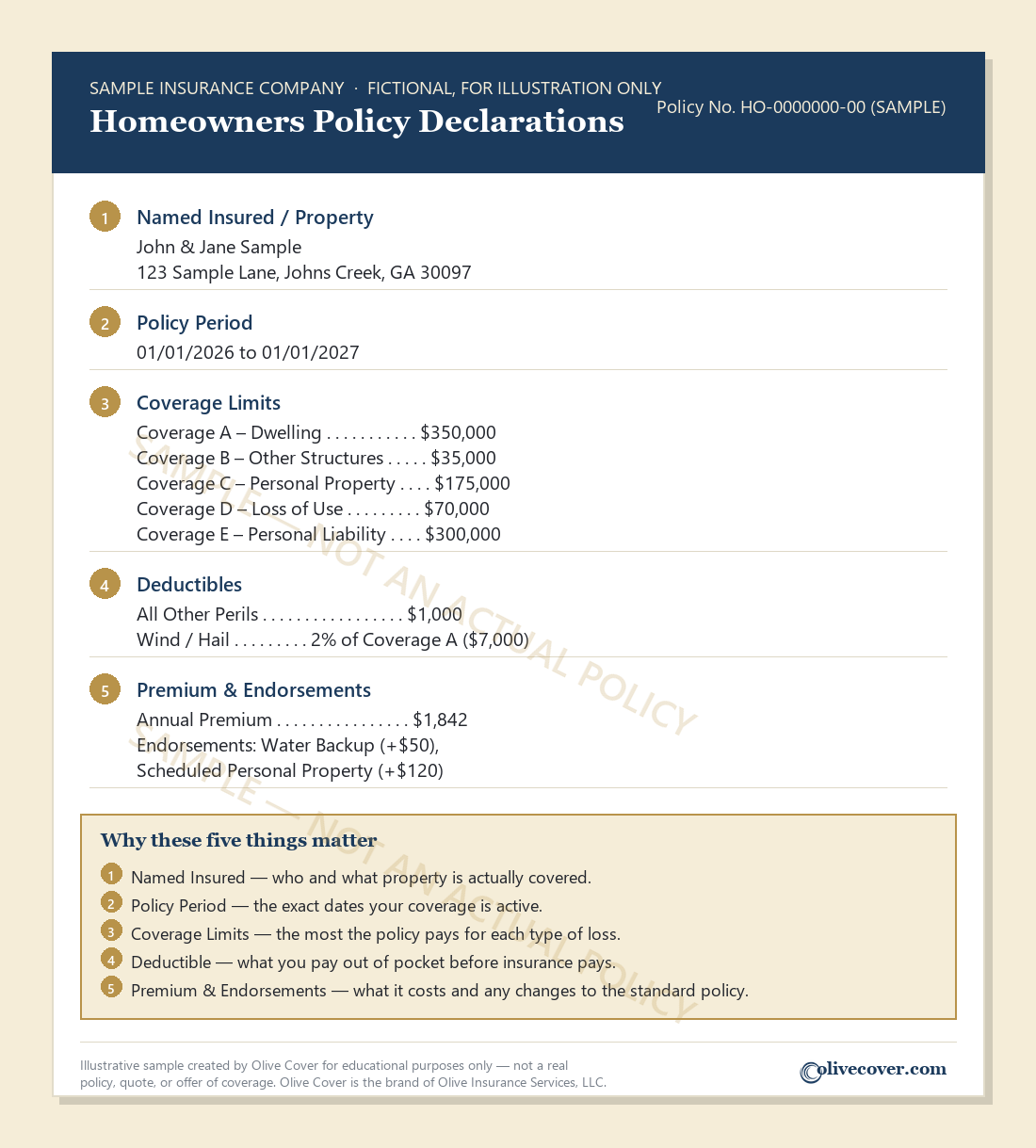

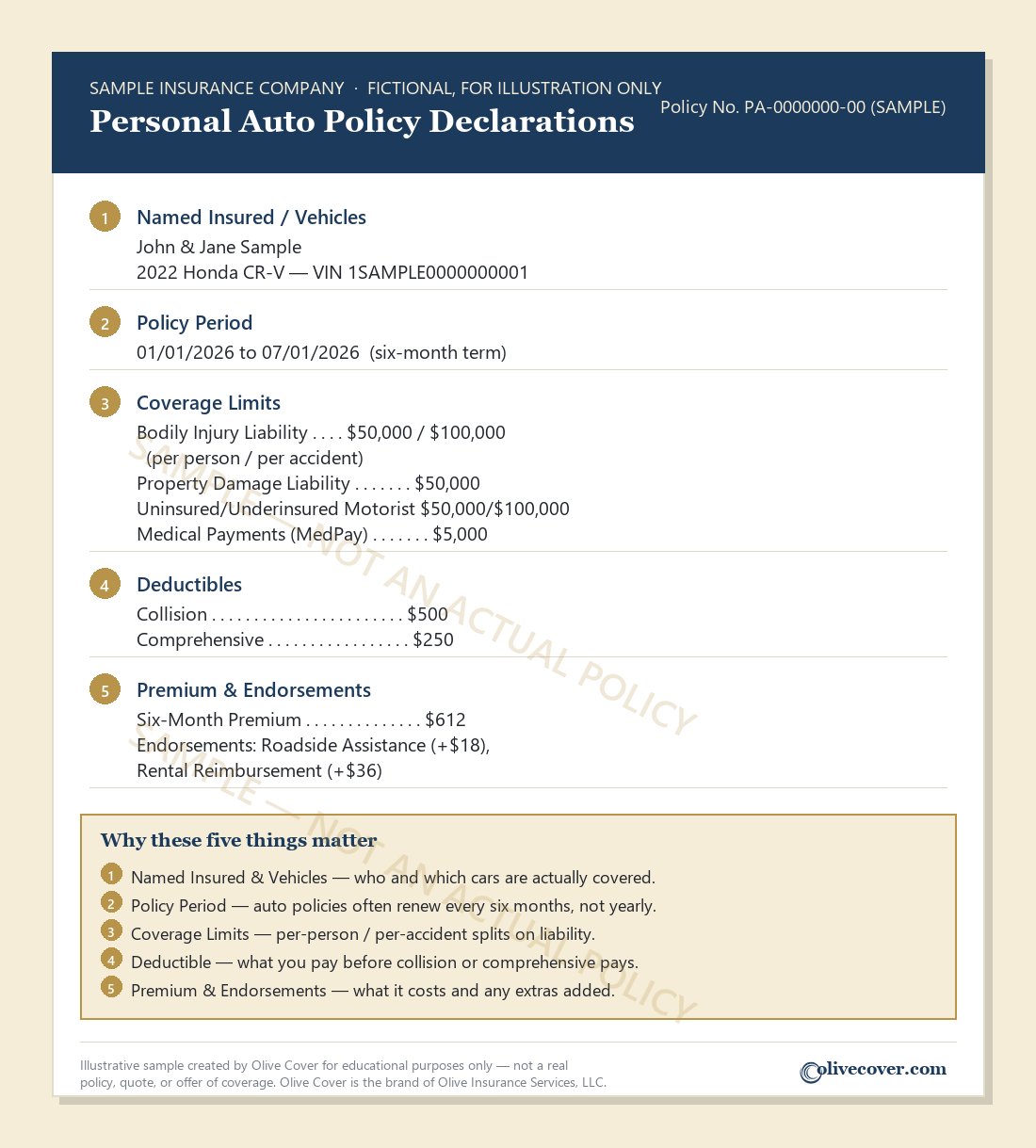

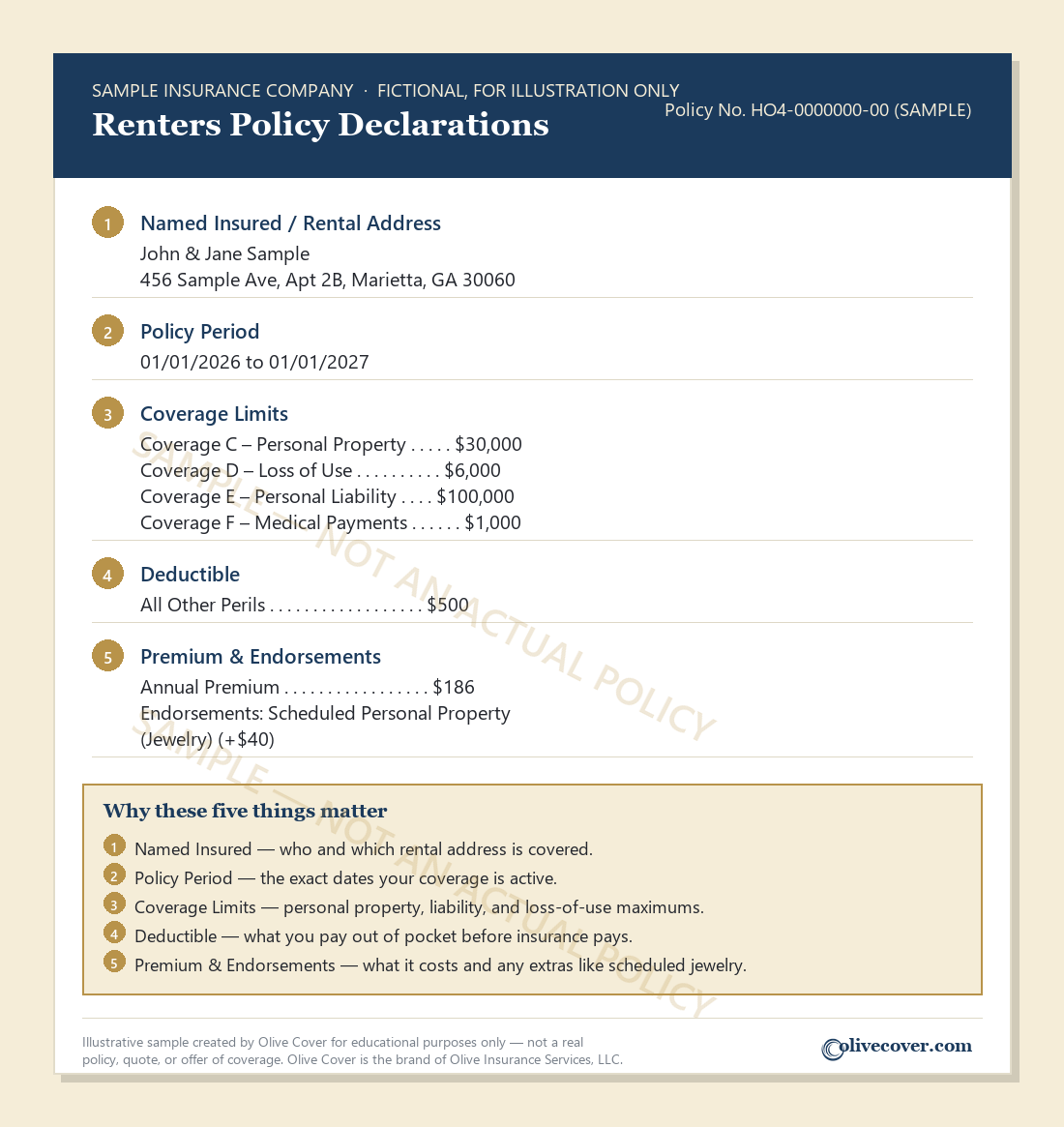

1. The named insured and address

At the top you will find the policyholder's name, the mailing address, and, for a home policy, the address of the insured property. For an auto policy, this section also lists every covered driver in the household. This matters more than people think. If your adult child moved home to Suwanee and started driving your car, but is not listed, a claim involving that driver can be denied. Always confirm the names and the property address are correct and complete.

2. The policy number and policy period

The policy number is your unique account reference. The policy period shows the exact start and end dates, almost always a 12 month term. Coverage applies only between those dates. If a pipe bursts the day after your policy lapses, you are on your own, so mark the renewal date on your calendar.

3. The coverage limits

This is the heart of the page. Limits are the maximum dollar amounts your insurer will pay for each type of loss. On a homeowners policy you will typically see several separate limits, often labeled Coverage A through Coverage F:

- Coverage A, Dwelling: the amount to rebuild your house itself.

- Coverage B, Other Structures: detached items like a fence, shed, or garage.

- Coverage C, Personal Property: your belongings, furniture, clothing, and electronics.

- Coverage D, Loss of Use: hotel and extra living costs if your home is unlivable.

- Coverage E, Personal Liability: protection if someone is hurt and you are responsible.

- Coverage F, Medical Payments: small medical bills for a guest injured on your property.

On an auto policy, the limits cover bodily injury liability, property damage liability, and optional pieces like collision and comprehensive. Understanding what each limit means is so important that it deserves its own attention. To go deeper on how rebuild (replacement) cost is calculated, see our guide to replacement cost versus actual cash value, and our overview of homeowners insurance.

4. The deductibles

Your deductible is the amount you pay out of pocket before insurance pays the rest. The dec page lists it for each coverage type. In Georgia you will often see two different deductibles on a home policy: a flat dollar deductible for most claims and a separate, usually higher, percentage deductible for wind and hail. We explain why that second number exists in our piece on Georgia wind and hail deductibles. If the term itself is fuzzy, our glossary entry on the deductible breaks it down plainly.

5. The premium

The premium is what you pay for the policy, shown as an annual total and sometimes broken into monthly or installment amounts. The dec page may also list fees and any discounts applied, such as bundling your home and auto.

6. Endorsements and forms

Near the bottom you will usually find a list of endorsements, also called riders, and the form numbers attached to your policy. An endorsement is an add-on that changes the standard coverage, either adding protection or limiting it. If you added scheduled coverage for an engagement ring or bought sewer backup protection, it shows up here. Learn more in our glossary entries on the endorsement and the exclusion.

7. The mortgagee or lienholder

If you have a mortgage or a car loan, your lender is listed as a mortgagee or loss payee. Lenders require this because they have a financial stake in the property. If you refinance or pay off the loan, make sure this section is updated.

A real-world walk-through

Consider a homeowner in Cumming whose dec page shows a Coverage A dwelling limit of $400,000, a Coverage C personal property limit of $200,000, a standard deductible of $1,000, and a 2 percent wind and hail deductible. A spring hailstorm, common across north Georgia, damages the roof and the rebuild estimate comes to $35,000. Because the wind and hail deductible is 2 percent of the $400,000 dwelling limit, the homeowner pays the first $8,000, not $1,000, and insurance covers the remaining $27,000. A homeowner who never read the dec page would be blindsided by that $8,000 number at the worst possible moment.

Now consider an Alpharetta family whose home would actually cost about $520,000 to rebuild today, given current north Atlanta construction costs, but whose dec page still shows a Coverage A limit of $400,000 from when they bought years ago. If a fire destroys the house, they could be short by roughly $120,000. This is exactly the gap we describe in why many north Atlanta homeowners are underinsured and in our list of common Georgia homeowners insurance gaps. The dec page is where you catch this, by comparing the dwelling limit to a current rebuild estimate.

On the auto side, picture a Duluth driver whose dec page shows bodily injury liability of 25/50, meaning $25,000 per person and $50,000 per accident. Those happen to be close to Georgia's required minimums, but a single serious accident can generate far higher medical bills. Reading the dec page is what prompts many drivers to raise those limits. Our guide to Georgia auto insurance minimum limits explains why the state minimum is rarely enough, and our auto insurance overview covers your options.

Renters follow the same logic on a smaller scale. Picture a Marietta renter whose dec page shows a Coverage C personal property limit of $30,000, a Coverage D loss-of-use limit of $6,000, and a $500 deductible. A kitchen fire in a neighboring unit forces a two-week hotel stay while smoke damage is cleaned from their apartment. The $6,000 loss-of-use limit covers the hotel and meals, and the $30,000 personal property limit replaces smoke-damaged clothing and furniture, minus the $500 deductible. A renter who never checked those numbers might assume, incorrectly, that renters insurance only covers theft.

Why the declarations page matters so much

The dec page is the fastest way to check whether your coverage still fits your life. People remodel kitchens, finish basements, buy jewelry, add drivers, and pay off mortgages, and the policy does not update itself. A five minute review once a year catches mismatches before they become claim denials or out of pocket shortfalls.

It is also the document the rest of the world asks for. Your mortgage company wants it to confirm coverage. A landlord may want proof of renters insurance. After a claim, the adjuster works from your limits and deductibles. When you compare quotes, lining up two dec pages side by side is the only honest apples-to-apples comparison, because a cheaper premium often hides lower limits or a higher deductible.

How to read yours in five minutes

- Confirm the names, drivers, and property address are correct and current.

- Check the dwelling limit against a realistic rebuild cost. Industry sources like CoreLogic note that construction costs have risen sharply, so older limits are often too low.

- Note every deductible, especially the separate wind and hail percentage.

- Read the endorsement list and ask what is missing, such as flood, which standard home policies exclude.

- Confirm the liability limits are high enough for your assets.

Common questions about declarations pages

Is the declarations page the same as the full policy?

No. The dec page summarizes your specific coverage, but the full policy contains the detailed rules, definitions, and exclusions. When they seem to conflict, the full policy language controls. Use the dec page to know your numbers and the policy to know the fine print.

What if something on my dec page is wrong?

Contact your agent right away. Errors in names, addresses, limits, or lienholders should be corrected immediately, because a claim could be challenged over a mismatch. It is far easier to fix a typo today than to argue about it after a loss.

Where do I find my dec page?

It arrives with your policy documents at purchase and again at each renewal, by mail or email, and it is usually available in your insurer's online account. Keep a copy somewhere you can reach it quickly, since it is the document you will want first after a fire, theft, or storm.

Does flood show up on it?

Standard homeowners policies in Georgia exclude flood, so it will not appear unless you bought a separate flood policy, which has its own dec page. Given how much of the state sits in flood-prone areas per FEMA mapping, this is a gap worth checking. See our comparison of NFIP versus private flood insurance and our flood insurance overview.

Let us review your declarations page with you

Your declarations page tells the story of how well you are actually protected, and most of the gaps that hurt Georgia families are hiding in plain sight on that one sheet. If you would like a second set of eyes, Olive Cover, the consumer brand of Olive Insurance Services, LLC, an independent property and casualty agency licensed in Georgia, will read it with you line by line and explain what each number means. We can compare your current limits to today's rebuild costs and flag anything missing. Request a free, no-pressure coverage review, and feel free to browse our insurance glossary or FAQ while you are here. To learn how this page fits with the rest of your paperwork, our companion article on understanding your policy documents ties it all together.